Candour Legal – Best Lawyers in Ahmedabad | Law firm in Ahmedabad

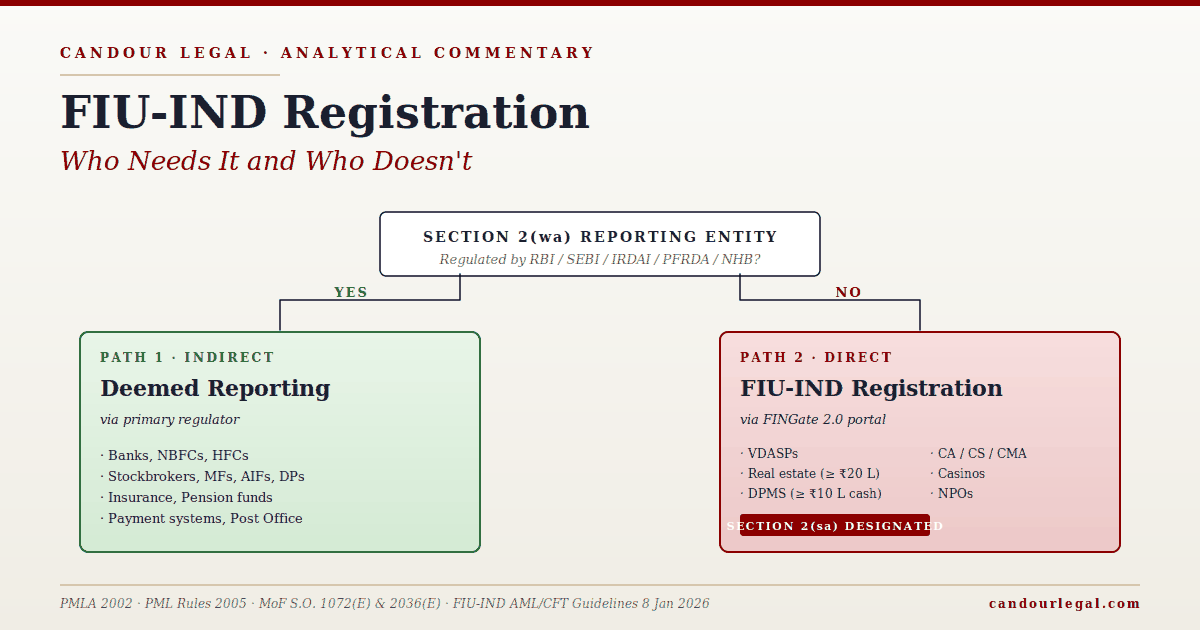

There are six categories of person or business that must register directly with the Financial Intelligence Unit — India (FIU-IND) under the Prevention of Money Laundering Act, 2002, and a much larger universe of regulated entities that satisfy the same statutory obligations through a different administrative pathway. The two are routinely conflated. The confusion produces three downstream errors that turn up in client intake every quarter: founders treating a “reporting entity” label as a licence to operate, regulated financial institutions investing in duplicative registration, and Designated Non-Financial Businesses and Professions failing to register at all because they assume “AML rules apply only to banks.” This piece sets out the categorical answer. It identifies who must register with FIU-IND directly, who reports through a primary regulator, what the registration mechanics actually look like, and what the penalty and enforcement architecture has done over the last twenty-four months.

Key Takeaways

- “Reporting entity” under Section 2(wa) of PMLA and “direct FIU-IND registrant” are not synonyms — the latter is a subset of the former.

- Six categories register with FIU-IND directly: VDASPs, real estate agents, DPMS, practising CA/CS/CMA, casinos, and NPOs.

- VDASP registration was triggered by Ministry of Finance Gazette Notification S.O. 1072(E) dated 7 March 2023 under Section 2(sa). It applies to offshore platforms serving Indian users — the Binance ₹18.82 crore and Bybit ₹9.27 crore penalty orders confirmed reach.

- The CA/CS/CMA designation under MoF Notification S.O. 2036(E) dated 3 May 2023 covers only six specified financial transactions carried out on behalf of a client. Pure audit, tax filing, and statutory certification work falls outside the scope.

- Real estate agents register at the ₹20 lakh transaction threshold (notification effective 17 May 2022); dealers in precious metals and stones at the ₹10 lakh cash-transaction threshold (December 2020).

- Banks, NBFCs, SEBI intermediaries, insurance companies, and pension funds are reporting entities but notify FIU-IND through their licensing regulator — they do not register separately.

- The Section 13 penalty range is ₹10,000–₹1,00,000 per violation; Section 70 imposes personal exposure on the Designated Director and any officer responsible for the company’s business at the time of the contravention.

The Two Paths to FIU Compliance

A reporting entity, under Section 2(1)(wa) of the Prevention of Money Laundering Act, 2002, is a banking company, financial institution, intermediary, or person carrying on a designated business or profession. The definition is wide and is the gateway to every Chapter IV obligation in the statute — recordkeeping under Section 12, customer identification, beneficial ownership identification, transaction reporting, and the five-year retention discipline. Reporting-entity status is the legal classification; FIU-IND registration is the administrative consequence in some, but not all, cases.

The administrative split runs on a single question. Is the entity already regulated by a primary financial-sector regulator — the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, or the National Housing Bank? If yes, the entity’s FIU-IND notification is routed through that regulator’s licensing pipeline. The bank, NBFC, stockbroker, insurer, or pension fund appoints a Designated Director and a Principal Officer, maintains the compliance programme architecture under Section 12, and files Suspicious Transaction Reports and the four other report types through FIU-IND’s portal — but the registration step itself is folded into the regulator’s authorisation framework.

If no, the entity is a “designated business or profession” under Section 2(sa) — and registers with FIU-IND directly. The six categories that fall into this second path are the ones that draw the bulk of FIU-IND’s recent enforcement attention, because each of them sits outside any pre-existing licensing framework and reaches the regulator only through the PMLA gateway.

Direct Registration Required: The Six Categories

Are you a Virtual Digital Asset Service Provider?

The Ministry of Finance, by Gazette Notification S.O. 1072(E) dated 7 March 2023, designated five categories of virtual digital asset activity as “designated business or profession” under Section 2(sa) of PMLA. An entity that carries on any of the five categories of activity, on behalf of another natural or legal person, in the course of business, becomes a reporting entity and must register with FIU-IND directly.

The five categories are: exchange between virtual digital assets and fiat currencies; exchange between one or more forms of virtual digital assets; transfer of virtual digital assets; safekeeping or administration of virtual digital assets, including instruments enabling control over them; and participation in and provision of financial services related to an issuer’s offer and sale of a virtual digital asset. The five categories track the FATF’s 2019 Recommendation 15 on virtual assets and virtual asset service providers.

Reach extends to offshore platforms providing services into India. The 2024–2025 enforcement record makes the point. The Binance order of June 2024 imposed a penalty of ₹18.82 crore and required compliance commitments before the platform’s return to the Indian market. The Bybit order of January 2025 imposed ₹9.27 crore. FIU-IND has issued show-cause notices to nine other offshore platforms and coordinated takedown directions through the Ministry of Electronics and Information Technology. The current operative AML/CFT framework for VDASPs is the FIU-IND Guidelines dated 8 January 2026.

Are you a real estate agent at the ₹20 lakh threshold?

Real estate agents were designated under PML Rules with the threshold operative from 17 May 2022. A person engaged in transactions of immovable property of ₹20 lakh or more, or its equivalent in foreign currency, is a reporting entity. The definition covers brokers, agents, intermediaries, and any person who acts as a conduit between buyer and seller of immovable property for consideration.

The Ahmedabad and surrounding commercial property market — the GIFT City catchment, Bopal–Shela–South Bopal corridor, Sanand industrial belt — sees a high concentration of transactions above the threshold. Registration penetration in this segment remains low; FIU-IND inspection volume has not yet caught up to what the registered population would otherwise suggest is appropriate.

Do you deal in precious metals or stones at ₹10 lakh cash?

Dealers in precious metals and precious stones were brought within PMLA reporting through a December 2020 designation. The threshold is ₹10 lakh or more in any cash transaction, or in a series of integrally connected cash transactions within a calendar month. The category covers jewellers, bullion dealers, diamond merchants, and any person dealing in cut and polished stones for trade or retail.

The Surat diamond cluster sits squarely within this designation. Registration discipline in the cluster has historically lagged the equivalent gold trade in Mumbai, and FIU-IND’s recent advisories have flagged the gap as a priority for the next inspection cycle.

Are you a practising CA, CS, or Cost Accountant doing one of these six things?

The Ministry of Finance, by Gazette Notification S.O. 2036(E) dated 3 May 2023, designated certain financial transactions carried out by Chartered Accountants, Company Secretaries, and Cost Accountants in practice as “designated business or profession” under PMLA. The designation is transaction-specific, not profession-wide.

A practising CA, CS, or Cost Accountant is a reporting entity only when, on behalf of a client, the professional carries out one or more of the following six transactions: buying and selling of immovable property; managing client money, securities, or other assets; management of bank, savings, or securities accounts; organisation of contributions for the creation, operation, or management of companies; creation, operation, or management of legal persons or arrangements; and buying and selling of business entities.

The corollary matters. Pure statutory audit, tax-return filing, statutory certification under the Companies Act 2013, GST advisory, and traditional management consulting are outside the scope. Privilege-and-confidentiality questions arise where the same professional acts in both capacities for the same client, and the institutional positions taken by the ICAI, ICSI, and ICMAI on this interface continue to evolve.

Casinos

Casinos were brought within the Section 2(sa) framework as part of the same broad sweep. In India, the practical footprint is limited — Goa, Sikkim, Daman, and offshore cruise operators with Indian itineraries. The casino operator is the reporting entity. Patron-side identity verification and source-of-funds documentation are the principal operational obligations. The category’s small population belies its inspection priority: FIU-IND treats casino reporting as a high-risk channel.

Non-Profit Organisations

Non-Profit Organisations are reporting entities under Section 2(sa). The reporting trigger is the receipt of contributions above the prescribed threshold within a calendar month, generating an NPO Transaction Report (NTR). The 2023 amendments tightened the NTR perimeter and brought a wider range of charitable, religious, and not-for-profit organisations into the reporting fold. Registration with FIU-IND is required where the NPO is engaged in the regular receipt of foreign contributions or domestic contributions above the threshold. The interface with the Foreign Contribution Regulation Act, 2010, and with the Income Tax exemption regime under Sections 11 and 12 of the Income-tax Act, 1961, is operationally relevant and requires careful sequencing.

Reporting via Primary Regulator: The Larger Universe

The bulk of India’s reporting-entity population reaches FIU-IND through a primary regulator. Banks (including foreign bank branches), Non-Banking Financial Companies, Housing Finance Companies, and Cooperative banks discharge their PMLA obligations through the Reserve Bank of India’s licensing and Master Direction framework. Payment system operators and authorised payment intermediaries — Payment Aggregators, Prepaid Payment Instrument issuers, and white-label ATM operators — route their compliance through the RBI’s payment-systems department.

Securities-market intermediaries — stockbrokers, sub-brokers, depository participants, mutual funds, portfolio managers, alternative investment funds, custodians, debenture trustees, credit-rating agencies, and merchant bankers — sit under SEBI’s Anti-Money Laundering Directions and the SEBI (Intermediaries) Regulations, 2008. Insurance companies, insurance agents, insurance brokers, and web aggregators route through IRDAI. Pension fund managers and Points of Presence under the National Pension System route through PFRDA. The Department of Posts handles Post Office Savings Bank reporting.

| Category | Primary Regulator | Direct FIU Registration? |

|---|---|---|

| Banks, NBFCs, HFCs | RBI / NHB | No |

| SEBI intermediaries | SEBI | No |

| Insurance | IRDAI | No |

| Pension fund managers | PFRDA | No |

| VDASPs | None — direct to FIU | YES |

| Real estate agents (≥ ₹20 L) | None — direct to FIU | YES |

| DPMS (≥ ₹10 L cash) | None — direct to FIU | YES |

| CA/CS/CMA in practice (6 specified transactions) | ICAI / ICSI / ICMAI (professional only) | YES |

| Casinos | State licensing only | YES |

| NPOs (above NTR threshold) | MoF (registration) + MHA (FCRA) | YES |

These regulated entities still appoint Designated Directors and Principal Officers, maintain the compliance programme architecture, and file STRs, CTRs, NTRs, CCRs, and CBWTRs through FIU-IND’s electronic portal. The difference is the absence of a separate FIU-IND registration step.

How the Registration Actually Works

The direct-registration pathway runs through FIU-IND’s FINGate 2.0 portal. The procedure is sequenced rather than parallel — each step gates the next, and skipping a step delays the entire timeline.

Step one is the appointment of the Designated Director and Principal Officer by board resolution. Step two is the entity-level registration submission on the FINGate portal, with the corporate identity documents, beneficial-ownership chain, and AML/CFT policy attached. Step three is FIU-IND’s preliminary scrutiny — typically two to three weeks for a complete and clean application. Step four is the Principal Officer registration on the same portal and the issuance of the Principal Officer Registration Number (PRN). Step five is the entity’s FIU Reporting Entity Identification (FIUREID) issuance. Step six is the acknowledgement of the applicable AML/CFT Guidelines — the VDA-specific Guidelines of 8 January 2026 for VDASPs; the general guidelines for DNFBPs. Step seven is the first test report filing, which closes the registration cycle.

Realistic end-to-end timelines: four to six weeks for a VDASP application, two to three weeks for a DNFBP application, and eight to ten weeks where the corporate structure includes offshore parents or layered beneficial ownership.

Penalty Architecture and Enforcement Trend

Section 13 of PMLA empowers the Director of FIU-IND to impose a monetary penalty between ₹10,000 and ₹1,00,000 for each failure under the Act or rules. The per-violation construction is operationally significant — penalty quantum scales with the number of contraventions, not their character. A reporting entity with twelve months of unfiled CTRs faces a different penalty calculation from one with a single missed STR.

Section 70 imposes the personal liability layer. Where a contravention is attributable to consent, connivance, or neglect of the Designated Director or of any officer responsible for the company’s business at the time, the personal exposure crystallises. The 2024–2025 enforcement cycle delivered the loudest signal yet — Binance ₹18.82 crore, Bybit ₹9.27 crore, multiple offshore platform show-cause notices, and a coordinated takedown directive through MeitY. The operational posture for direct registrants in 2026 should reflect that signal: a sturdier compliance programme, sharper documentation, an enterprise-wide risk assessment that genuinely informs resource allocation, and a defensible audit trail.

Looking Ahead

Three trajectories deserve tracking over the next eighteen to twenty-four months. The first is the FATF mutual evaluation cycle’s effect on Indian PMLA design — the next round is expected to drive further sectoral inclusions, likely in the digital lending, real-money online gaming, and cross-border remittance segments. The second is the FINGate 2.0 platform’s migration toward structured beneficial-ownership data ingestion, which will demand reporting entities upgrade their underlying KYC and beneficial-ownership datasets — a non-trivial capital expense for mid-sized reporting entities. The third is the collision point between the Digital Personal Data Protection Act, 2023, and PMLA’s customer-data retention requirements; whether the tipping-off protections under Section 12(2) of PMLA override the consent-and-erasure framework under the DPDP Act remains an open question that will require either statutory clarification or judicial guidance in 2026 or 2027.

Frequently Asked Questions

Do all crypto exchanges need FIU registration even if they’re based outside India?

Yes, where the exchange offers services to Indian users in the course of business. The 7 March 2023 notification applies to the activity, not the place of incorporation. FIU-IND has demonstrated reach through the Binance and Bybit enforcement orders and through coordinated platform takedowns. An offshore exchange operating an Indian-language interface, accepting INR transactions, or marketing to Indian users falls within the registration requirement.

Does a Chartered Accountant doing pure tax filing need FIU registration?

No. The 3 May 2023 notification designates only the six specified financial transactions enumerated in the notification. Pure statutory audit, tax-return filing, GST advisory, statutory certification, and traditional management consulting are outside the designation. A CA who only files returns and prepares audit reports is not a reporting entity under PMLA.

What is the difference between being a “reporting entity” and “registering with FIU-IND”?

A reporting entity under Section 2(1)(wa) of PMLA is any entity that satisfies Chapter IV compliance obligations. Registration with FIU-IND is a separate administrative step required only for entities that lack a primary financial-sector regulator. A bank is a reporting entity but does not register separately with FIU-IND; a crypto exchange is both a reporting entity and a direct registrant.

Are all NBFCs required to register separately with FIU-IND?

No. NBFCs are licensed and supervised by the Reserve Bank of India. Their PMLA compliance is routed through the RBI’s Master Direction on KYC and the RBI’s licensing framework. They appoint a Designated Director and Principal Officer and file all five report types, but they do not register separately with FIU-IND.

What is the penalty for operating without FIU-IND registration when required?

Section 13 of PMLA permits a penalty between ₹10,000 and ₹1,00,000 per violation. The per-violation construction means that a sustained period of unregistered operation can accumulate substantial liability. Section 70 imposes personal exposure on the Designated Director and on any officer responsible for the company’s business. The Binance and Bybit orders illustrate the upper end of practical exposure for offshore VDA operators.

Can a real estate agent handle one ₹19 lakh transaction without triggering FIU obligations?

The reporting threshold for real estate agents is set at transactions of ₹20 lakh or more. A single transaction below the threshold does not trigger reporting on its face. Integrally connected transactions within the same calendar month and customer cluster aggregate to the threshold under the standard PMLA interpretation. Structuring a transaction at ₹19 lakh to defeat the threshold is itself a red flag and an STR trigger.

Is there a single FIU-IND ID for multi-category intermediaries?

Not yet. FIU-IND has indicated that a single-FIUREID model for stock-market intermediaries operating in multiple SEBI-registered categories is under consideration, but the implementation has not been notified. As of June 2026, an intermediary holding multiple SEBI registrations must obtain a separate FIUREID for each category.

Further reading

- Building the FIU-IND Compliance Programme: A Designated Director’s Playbook — the operational architecture once you are a registered reporting entity.

- FIU-IND Registration for Crypto Businesses — the VDA-specific registration walkthrough.

- FIU-IND Registration Process and Documents — the procedural and documentary checklist.

- VDASP AML Compliance and Enforcement — the post-registration compliance and enforcement perspective.

BEFORE YOU GO

Get a free 15-minute case assessment

Tell us what’s going on and a Candour Legal advocate will call you back — no charge, no obligation.

Schedule my free assessment Call now

BEFORE YOU GO

Get a free 15-minute case assessment

Tell us what's going on and a Candour Legal advocate will call you back — no charge, no obligation.

Schedule my free assessment Call now